Fucking hell man, admit your mistake.

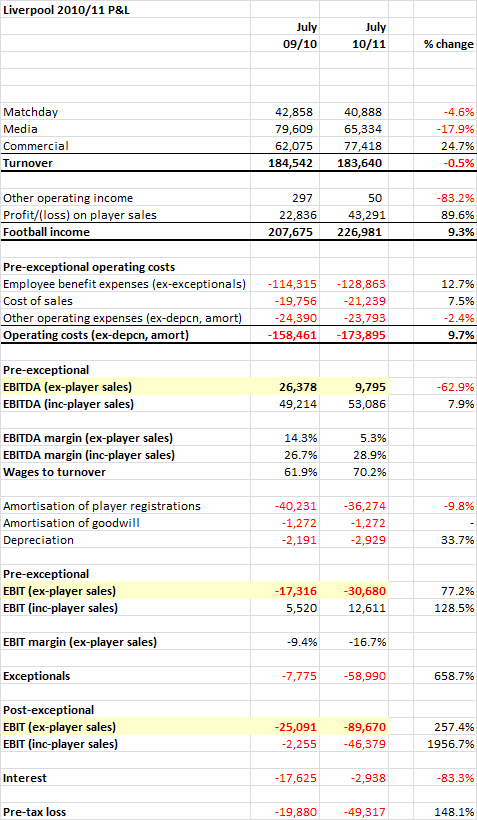

Total Football Income: £227m

Total Football Income: £227m

Is it right to assume that players, at cost, would be included in the balance sheet as assets, and the profit/loss on sale included in the P & L account?

I assume amortisation of player registrations is the devaluing of players as their contracts run out.

And our turnover last year was 180 something- which included 50m from the sale of Torres.

So without that sale or wage bill almost equals our turnover.

#thingsarentasrosyasomepeoplethink

I assume amortisation of player registrations is the devaluing of players as their contracts run out.

We've had all this before ages ago and I was wrong, as usual. But I can't remember how wrong or what I thought was right in the first place.

Glad to be of help.

I appreciate that the value of a player in the balance sheet would be depreciated. The point I was trying to clarify was that, I would have thought, only the profit/loss on a player would appear in the P & L account. That is the profit/loss on the written down value of the player.

For example we sold Torres for 50m but that is not the figure that would appear in the accounts. The proper figure would be the profit based on his WDV. Or is that completely wrong?

Would think it's down substantially for the year ended July 2013, probably by at least £15m or so.

Nope. G&H put in 150m that they borrowed personally - nothing to do with the club. It's that 150m that they're suing for now. That money covered the interest + overspending on players.

FSG put in 30m of their own money last year for transfer spending.

Who was it who said it wasn't going to court because we couldn't stump up the £1m in fees?

Oh. More unsubstantiated selective insider bollocks.

If you need to talk....athensrauri can point you in the general direction of someone.Haha...I'm quitting while I'm behind.

Well fuck a duck! that sounds like a payout to me, i would be very surprised if those mentioned could make a large payout so I wonder whats gone on. Weird.